BOE-A-2025-27116 was published in the Official State Gazette. This regulation establishes the obligation to submit an annual information form detailing stays during the year 2025.

Content

This reporting model is an annual system that transforms daily operations (reservations, actual check-in and check-out dates, number of guests, and purpose of stay) into a structured declaration by property and by rental unit . It aligns with the European framework that promotes the collection and exchange of data on short-term rentals, strengthening transparency and control over tourism activity.

The obligation to report on tourist rentals already existed through other models and regulations, but the 2026 deadline marks the full implementation of this specific annual model and its integration into the Single Registry and the Digital One-Stop Shop for Rentals. For managers, this means a clear timeline (February as the key month) and a standardized reporting format, which reduces discretion and increases the traceability of the information reported.

It is essential to distinguish between holiday rentals and other seasonal rentals, since the model focuses on short-term rentals , especially those marketed through online platforms and with a specific tourist or temporary purpose.

The information template includes information about your bookings : the purpose of the rental , number of guests , the check-in and check-out dates for each stay , and details related to your property .

In practice, each manager must be able to clearly link the property to the different operating units that are marketed (for example, different apartments or internal references), so that the report accurately reflects what has been rented and in what periods.

The general rule is fixed: the form must be submitted during the month of February and the deadline is March 2nd. Reservation records or rental deposits must be submitted in CSV format using the Land Registry's N2 application.

The information is organized into three main sections: (1) identification of the applicant, (2) identification of the property, and (3) details of the activity for each rental unit. This third section includes a declaration of stays during the previous calendar year , with the minimum level of detail required by the regulations.

For managers , this means having all properties inventoried with their CRU and having a system that allows extracting and consolidating activity data per rental unit, without contradictions between what is commercially exploited and what is declared in the registry.

For each lease unit, the model requires a minimum set of fields that must be extractable from daily operations. These include:

These fields convert daily bookings and stays into a structured annual record, so the quality of the data in check-in and booking management is crucial for a correct and trouble-free deposit.

The registrars' association warns that the consequences of not submitting the form on time and in the correct manner may lead to the revocation of the Unique Rental Registration Number (NRUA) .

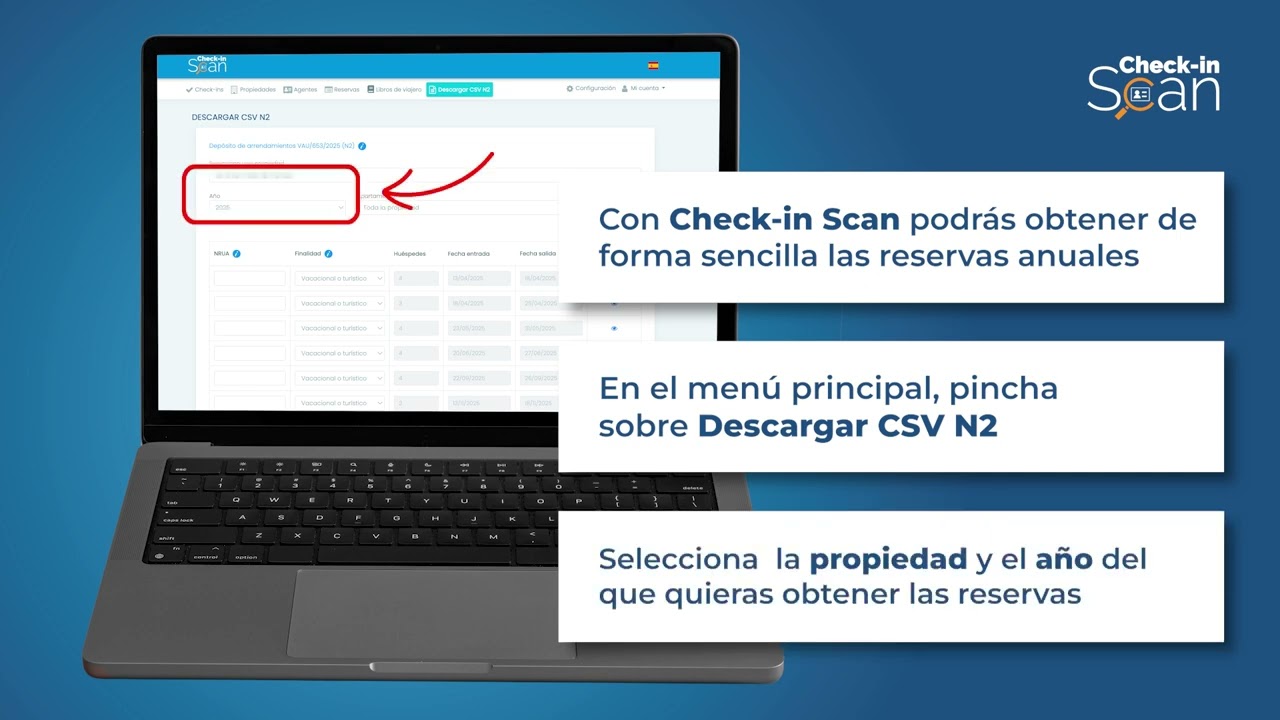

Below we explain how to download the CSV file of the reservations made at your property, which you can attach to the N2 application of the Property Registry.

Access your account's web control panel, go to the "Download CSV N2" and select the property you wish to manage.

Next, enable the “Generate CSV N2” . A list will then be displayed showing all reservations made throughout 2025 at the selected property.

You must indicate the NRUA (Unique Rental Registration Number) of the property at least in the first booking, so that the system collects it and automatically fills in that field in all of them.

All reservations in the listing correspond to the same property, so the NRUA will be the same for all of them and you don't need to write it one by one.

Once you have verified that all the information is correct, click on the orange button: “Generate CSV N2” .

The document will be automatically downloaded in CSV format. This file meets the format and requirements of the N2 application, so you can attach it to the application to automatically fill in reservation details.

If you prefer to export the reservation list in Excel format, we also have this option available.

Access your account's web control panel

Once inside, go to the “Check-ins” section. In the upper right corner of the panel, you will find the “Export bookings” option.

Click on it and select the property and date range from which you want to export the bookings.

The system will generate an Excel file in which you can find a list with the locator, check-in and check-out dates and number of guests for all reservations made at the property and selected date period.

This will help you complete the new information model for reservations ( VAU/1560/2025).

IMPORTANT : The system used to open the Excel file sets all columns to the same width by default. For this reason, you may not be able to correctly view the check-in and check-out dates for reservations, as the text length exceeds the width. To resolve this, you need to manually increase the width of the corresponding columns.

Jorge Ortiz says:

What could happen if I don't send the reservations?

Support Team says:

Hi Jorge, thank you so much for joining the conversation. If you don't submit the reservations on time and correctly, you risk losing the NRUA (Registered Tourist Accommodation Registration) for your tourist accommodation.

Consuelo Algora says:

I am the owner with regional authorization of a tourist apartment and NRUA, rented to my son who sublets and rents it in the summer, he is the one who manages it and collects the rent.

Support Team says:

Hello Consuelo! Regarding your inquiry, we would like to inform you that, when dealing with specific cases or legal matters, we always recommend that you consult with your property manager or lawyer, or contact the Land Registry directly, as we cannot offer legal advice on this matter.

However, based on the information we have, we can confirm that the Rental Deposit can be submitted by either the owner or the property manager.

Furthermore, please note that the Rental Deposit is not related to the Tax Agency, so it is irrelevant who receives the payment.

Greetings and thank you.